VOTING POWER100.00%

DOWNVOTE POWER100.00%

RESOURCE CREDITS100.00%

REPUTATION PROGRESS0.00%

Net Worth

0.007USD

STEEM

0.000STEEM

SBD

0.000SBD

Effective Power

5.007SP

├── Own SP

0.125SP

└── Incoming DelegationsDeleg

+4.883SP

Detailed Balance

| STEEM | ||

| balance | 0.000STEEM | STEEM |

| market_balance | 0.000STEEM | STEEM |

| savings_balance | 0.000STEEM | STEEM |

| reward_steem_balance | 0.000STEEM | STEEM |

| STEEM POWER | ||

| Own SP | 0.125SP | SP |

| Delegated Out | 0.000SP | SP |

| Delegation In | 4.883SP | SP |

| Effective Power | 5.007SP | SP |

| Reward SP (pending) | 0.000SP | SP |

| SBD | ||

| sbd_balance | 0.000SBD | SBD |

| sbd_conversions | 0.000SBD | SBD |

| sbd_market_balance | 0.000SBD | SBD |

| savings_sbd_balance | 0.000SBD | SBD |

| reward_sbd_balance | 0.000SBD | SBD |

{

"balance": "0.000 STEEM",

"savings_balance": "0.000 STEEM",

"reward_steem_balance": "0.000 STEEM",

"vesting_shares": "202.836552 VESTS",

"delegated_vesting_shares": "0.000000 VESTS",

"received_vesting_shares": "7940.823254 VESTS",

"sbd_balance": "0.000 SBD",

"savings_sbd_balance": "0.000 SBD",

"reward_sbd_balance": "0.000 SBD",

"conversions": []

}Account Info

| name | suweenja |

| id | 1077456 |

| rank | 287,035 |

| reputation | 9507958 |

| created | 2018-07-16T19:48:18 |

| recovery_account | steem |

| proxy | None |

| post_count | 2 |

| comment_count | 0 |

| lifetime_vote_count | 0 |

| witnesses_voted_for | 0 |

| last_post | 2018-08-09T15:41:03 |

| last_root_post | 2018-08-09T15:41:03 |

| last_vote_time | 2018-08-13T15:34:39 |

| proxied_vsf_votes | 0, 0, 0, 0 |

| can_vote | 1 |

| voting_power | 0 |

| delayed_votes | 0 |

| balance | 0.000 STEEM |

| savings_balance | 0.000 STEEM |

| sbd_balance | 0.000 SBD |

| savings_sbd_balance | 0.000 SBD |

| vesting_shares | 202.836552 VESTS |

| delegated_vesting_shares | 0.000000 VESTS |

| received_vesting_shares | 7940.823254 VESTS |

| reward_vesting_balance | 0.000000 VESTS |

| vesting_balance | 0.000 STEEM |

| vesting_withdraw_rate | 0.000000 VESTS |

| next_vesting_withdrawal | 1969-12-31T23:59:59 |

| withdrawn | 0 |

| to_withdraw | 0 |

| withdraw_routes | 0 |

| savings_withdraw_requests | 0 |

| last_account_recovery | 1970-01-01T00:00:00 |

| reset_account | null |

| last_owner_update | 1970-01-01T00:00:00 |

| last_account_update | 1970-01-01T00:00:00 |

| mined | No |

| sbd_seconds | 0 |

| sbd_last_interest_payment | 1970-01-01T00:00:00 |

| savings_sbd_last_interest_payment | 1970-01-01T00:00:00 |

{

"id": 1077456,

"name": "suweenja",

"owner": {

"weight_threshold": 1,

"account_auths": [],

"key_auths": [

[

"STM5ZrKg3FW3GHBPchfVx5uskqrSjKvjW4f9ksoQweVYj1v64aiew",

1

]

]

},

"active": {

"weight_threshold": 1,

"account_auths": [],

"key_auths": [

[

"STM6xWbFtE1aC7Q4LiK6YqTLvAAcgSQXHPZEpn4HJo667rUmJqREW",

1

]

]

},

"posting": {

"weight_threshold": 1,

"account_auths": [],

"key_auths": [

[

"STM6mekbfXs56BDwGbUecDTNbA8RPt4y1kLG9vBy9MFinbRk81T2n",

1

]

]

},

"memo_key": "STM798NxsfK62zCz3YApekgH3PBgibcfuYKJFgiryy1yzGYSsi4mr",

"json_metadata": "{}",

"posting_json_metadata": "",

"proxy": "",

"last_owner_update": "1970-01-01T00:00:00",

"last_account_update": "1970-01-01T00:00:00",

"created": "2018-07-16T19:48:18",

"mined": false,

"recovery_account": "steem",

"last_account_recovery": "1970-01-01T00:00:00",

"reset_account": "null",

"comment_count": 0,

"lifetime_vote_count": 0,

"post_count": 2,

"can_vote": true,

"voting_manabar": {

"current_mana": "8143659806",

"last_update_time": 1779087903

},

"downvote_manabar": {

"current_mana": 2035914951,

"last_update_time": 1779087903

},

"voting_power": 0,

"balance": "0.000 STEEM",

"savings_balance": "0.000 STEEM",

"sbd_balance": "0.000 SBD",

"sbd_seconds": "0",

"sbd_seconds_last_update": "1970-01-01T00:00:00",

"sbd_last_interest_payment": "1970-01-01T00:00:00",

"savings_sbd_balance": "0.000 SBD",

"savings_sbd_seconds": "0",

"savings_sbd_seconds_last_update": "1970-01-01T00:00:00",

"savings_sbd_last_interest_payment": "1970-01-01T00:00:00",

"savings_withdraw_requests": 0,

"reward_sbd_balance": "0.000 SBD",

"reward_steem_balance": "0.000 STEEM",

"reward_vesting_balance": "0.000000 VESTS",

"reward_vesting_steem": "0.000 STEEM",

"vesting_shares": "202.836552 VESTS",

"delegated_vesting_shares": "0.000000 VESTS",

"received_vesting_shares": "7940.823254 VESTS",

"vesting_withdraw_rate": "0.000000 VESTS",

"next_vesting_withdrawal": "1969-12-31T23:59:59",

"withdrawn": 0,

"to_withdraw": 0,

"withdraw_routes": 0,

"curation_rewards": 0,

"posting_rewards": 0,

"proxied_vsf_votes": [

0,

0,

0,

0

],

"witnesses_voted_for": 0,

"last_post": "2018-08-09T15:41:03",

"last_root_post": "2018-08-09T15:41:03",

"last_vote_time": "2018-08-13T15:34:39",

"post_bandwidth": 0,

"pending_claimed_accounts": 0,

"vesting_balance": "0.000 STEEM",

"reputation": 9507958,

"transfer_history": [],

"market_history": [],

"post_history": [],

"vote_history": [],

"other_history": [],

"witness_votes": [],

"tags_usage": [],

"guest_bloggers": [],

"rank": 287035

}Withdraw Routes

| Incoming | Outgoing |

|---|---|

Empty | Empty |

{

"incoming": [],

"outgoing": []

}From Date

To Date

2026/05/18 07:05:03

2026/05/18 07:05:03

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 7940.823254 VESTS |

| Transaction Info | Block #106151611/Trx 96c5c6e97883562418acee18e8866dab1c2f8203 |

View Raw JSON Data

{

"trx_id": "96c5c6e97883562418acee18e8866dab1c2f8203",

"block": 106151611,

"trx_in_block": 7,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2026-05-18T07:05:03",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "7940.823254 VESTS"

}

]

}2026/05/13 07:36:15

2026/05/13 07:36:15

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 5228.612849 VESTS |

| Transaction Info | Block #106008950/Trx 62d0d5624dcad51f521ac4eedf52195d5e4a404a |

View Raw JSON Data

{

"trx_id": "62d0d5624dcad51f521ac4eedf52195d5e4a404a",

"block": 106008950,

"trx_in_block": 1,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2026-05-13T07:36:15",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "5228.612849 VESTS"

}

]

}2026/04/26 06:15:42

2026/04/26 06:15:42

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 7953.339010 VESTS |

| Transaction Info | Block #105519074/Trx a3ff3039df75c8a271758582c3c8327f964af134 |

View Raw JSON Data

{

"trx_id": "a3ff3039df75c8a271758582c3c8327f964af134",

"block": 105519074,

"trx_in_block": 1,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2026-04-26T06:15:42",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "7953.339010 VESTS"

}

]

}2026/01/24 02:11:30

2026/01/24 02:11:30

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 5270.159668 VESTS |

| Transaction Info | Block #102873841/Trx 7c708f90af81704c95f8eb2f4a2c0d77b713fbc0 |

View Raw JSON Data

{

"trx_id": "7c708f90af81704c95f8eb2f4a2c0d77b713fbc0",

"block": 102873841,

"trx_in_block": 2,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2026-01-24T02:11:30",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "5270.159668 VESTS"

}

]

}2024/12/17 21:20:51

2024/12/17 21:20:51

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 5434.378865 VESTS |

| Transaction Info | Block #91320042/Trx 46560238ebd4df5c3db558fdba8c5663f8db865c |

View Raw JSON Data

{

"trx_id": "46560238ebd4df5c3db558fdba8c5663f8db865c",

"block": 91320042,

"trx_in_block": 1,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2024-12-17T21:20:51",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "5434.378865 VESTS"

}

]

}2023/11/14 13:00:30

2023/11/14 13:00:30

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 5603.512397 VESTS |

| Transaction Info | Block #79874153/Trx ffbbf933967a77546655ee18d4b65591a1d6a1b9 |

View Raw JSON Data

{

"trx_id": "ffbbf933967a77546655ee18d4b65591a1d6a1b9",

"block": 79874153,

"trx_in_block": 0,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2023-11-14T13:00:30",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "5603.512397 VESTS"

}

]

}2023/09/22 11:20:15

2023/09/22 11:20:15

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 8540.421183 VESTS |

| Transaction Info | Block #78363995/Trx 5915e12851bc63f46d6c1ddadba57532f1edb8a5 |

View Raw JSON Data

{

"trx_id": "5915e12851bc63f46d6c1ddadba57532f1edb8a5",

"block": 78363995,

"trx_in_block": 7,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2023-09-22T11:20:15",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "8540.421183 VESTS"

}

]

}2022/11/03 18:41:03

2022/11/03 18:41:03

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 8762.472621 VESTS |

| Transaction Info | Block #69121598/Trx 10cf73903b263a5e075120901b827953b5a9a647 |

View Raw JSON Data

{

"trx_id": "10cf73903b263a5e075120901b827953b5a9a647",

"block": 69121598,

"trx_in_block": 5,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2022-11-03T18:41:03",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "8762.472621 VESTS"

}

]

}2022/01/17 23:48:06

2022/01/17 23:48:06

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 8982.580222 VESTS |

| Transaction Info | Block #60824753/Trx b6217eef9920e92ffc33b509c3b1c7946df9391a |

View Raw JSON Data

{

"trx_id": "b6217eef9920e92ffc33b509c3b1c7946df9391a",

"block": 60824753,

"trx_in_block": 25,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2022-01-17T23:48:06",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "8982.580222 VESTS"

}

]

}2021/06/14 06:56:57

2021/06/14 06:56:57

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 9166.774510 VESTS |

| Transaction Info | Block #54615032/Trx 5443ba9b631801838cbd42f6c82ad385bad8709b |

View Raw JSON Data

{

"trx_id": "5443ba9b631801838cbd42f6c82ad385bad8709b",

"block": 54615032,

"trx_in_block": 6,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2021-06-14T06:56:57",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "9166.774510 VESTS"

}

]

}2020/12/11 17:08:36

2020/12/11 17:08:36

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 9354.196484 VESTS |

| Transaction Info | Block #49362274/Trx 0f36121ffd43502655bdf853bac30a022eb92f31 |

View Raw JSON Data

{

"trx_id": "0f36121ffd43502655bdf853bac30a022eb92f31",

"block": 49362274,

"trx_in_block": 4,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2020-12-11T17:08:36",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "9354.196484 VESTS"

}

]

}2020/12/06 10:43:54

2020/12/06 10:43:54

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 1912.543513 VESTS |

| Transaction Info | Block #49213783/Trx bc54ef42e9829ce6ce6a1c683969be09bae02602 |

View Raw JSON Data

{

"trx_id": "bc54ef42e9829ce6ce6a1c683969be09bae02602",

"block": 49213783,

"trx_in_block": 0,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2020-12-06T10:43:54",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "1912.543513 VESTS"

}

]

}2020/12/05 20:46:27

2020/12/05 20:46:27

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 9360.404338 VESTS |

| Transaction Info | Block #49197360/Trx e3a9068e2deff5d6bc241f8a0ba9e734945ee6bf |

View Raw JSON Data

{

"trx_id": "e3a9068e2deff5d6bc241f8a0ba9e734945ee6bf",

"block": 49197360,

"trx_in_block": 3,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2020-12-05T20:46:27",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "9360.404338 VESTS"

}

]

}2020/11/03 04:10:09

2020/11/03 04:10:09

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 1920.017158 VESTS |

| Transaction Info | Block #48272555/Trx bfcdeba3a8d6ca55250afe6cf7c7b15388bdfbc4 |

View Raw JSON Data

{

"trx_id": "bfcdeba3a8d6ca55250afe6cf7c7b15388bdfbc4",

"block": 48272555,

"trx_in_block": 1,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2020-11-03T04:10:09",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "1920.017158 VESTS"

}

]

}2020/05/09 11:47:48

2020/05/09 11:47:48

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 9563.209697 VESTS |

| Transaction Info | Block #43224129/Trx 07ae77ff91b87614449203b1e8bb06f7157f1338 |

View Raw JSON Data

{

"trx_id": "07ae77ff91b87614449203b1e8bb06f7157f1338",

"block": 43224129,

"trx_in_block": 26,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2020-05-09T11:47:48",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "9563.209697 VESTS"

}

]

}2020/05/08 16:18:12

2020/05/08 16:18:12

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 1953.311140 VESTS |

| Transaction Info | Block #43201293/Trx a56197722c3de1efc52830df7ab84329d12a377c |

View Raw JSON Data

{

"trx_id": "a56197722c3de1efc52830df7ab84329d12a377c",

"block": 43201293,

"trx_in_block": 3,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2020-05-08T16:18:12",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "1953.311140 VESTS"

}

]

}2019/11/01 09:42:48

2019/11/01 09:42:48

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 9669.608780 VESTS |

| Transaction Info | Block #37790433/Trx f3ab149d056d1489cf088c32d27a140c96cc45b1 |

View Raw JSON Data

{

"trx_id": "f3ab149d056d1489cf088c32d27a140c96cc45b1",

"block": 37790433,

"trx_in_block": 0,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-11-01T09:42:48",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "9669.608780 VESTS"

}

]

}2019/07/16 21:01:30

2019/07/16 21:01:30

| parent author | suweenja |

| parent permlink | 26yufg-arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives |

| author | steemitboard |

| permlink | steemitboard-notify-suweenja-20190716t210131000z |

| title | |

| body | Congratulations @suweenja! You received a personal award! <table><tr><td>https://steemitimages.com/70x70/http://steemitboard.com/@suweenja/birthday1.png</td><td>Happy Birthday! - You are on the Steem blockchain for 1 year!</td></tr></table> <sub>_You can view [your badges on your Steem Board](https://steemitboard.com/@suweenja) and compare to others on the [Steem Ranking](https://steemitboard.com/ranking/index.php?name=suweenja)_</sub> ###### [Vote for @Steemitboard as a witness](https://v2.steemconnect.com/sign/account-witness-vote?witness=steemitboard&approve=1) to get one more award and increased upvotes! |

| json metadata | {"image":["https://steemitboard.com/img/notify.png"]} |

| Transaction Info | Block #34722584/Trx 0bc9117a7a0e46aac244c0d9dcef10fd6ae5db46 |

View Raw JSON Data

{

"trx_id": "0bc9117a7a0e46aac244c0d9dcef10fd6ae5db46",

"block": 34722584,

"trx_in_block": 46,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-07-16T21:01:30",

"op": [

"comment",

{

"parent_author": "suweenja",

"parent_permlink": "26yufg-arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives",

"author": "steemitboard",

"permlink": "steemitboard-notify-suweenja-20190716t210131000z",

"title": "",

"body": "Congratulations @suweenja! You received a personal award!\n\n<table><tr><td>https://steemitimages.com/70x70/http://steemitboard.com/@suweenja/birthday1.png</td><td>Happy Birthday! - You are on the Steem blockchain for 1 year!</td></tr></table>\n\n<sub>_You can view [your badges on your Steem Board](https://steemitboard.com/@suweenja) and compare to others on the [Steem Ranking](https://steemitboard.com/ranking/index.php?name=suweenja)_</sub>\n\n\n###### [Vote for @Steemitboard as a witness](https://v2.steemconnect.com/sign/account-witness-vote?witness=steemitboard&approve=1) to get one more award and increased upvotes!",

"json_metadata": "{\"image\":[\"https://steemitboard.com/img/notify.png\"]}"

}

]

}2018/11/26 19:39:33

2018/11/26 19:39:33

| delegator | steem |

| delegatee | suweenja |

| vesting shares | 9867.084157 VESTS |

| Transaction Info | Block #28046532/Trx 7b32041f04e7f7580c929ba5d56025328cb8f2da |

View Raw JSON Data

{

"trx_id": "7b32041f04e7f7580c929ba5d56025328cb8f2da",

"block": 28046532,

"trx_in_block": 14,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2018-11-26T19:39:33",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "suweenja",

"vesting_shares": "9867.084157 VESTS"

}

]

}2018/08/13 15:34:39

2018/08/13 15:34:39

| voter | suweenja |

| author | suweenja |

| permlink | 26yufg-arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives |

| weight | 10000 (100.00%) |

| Transaction Info | Block #25035220/Trx 64b0d050654d4873e699a1afe30fafb5b275bf5c |

View Raw JSON Data

{

"trx_id": "64b0d050654d4873e699a1afe30fafb5b275bf5c",

"block": 25035220,

"trx_in_block": 24,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2018-08-13T15:34:39",

"op": [

"vote",

{

"voter": "suweenja",

"author": "suweenja",

"permlink": "26yufg-arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives",

"weight": 10000

}

]

}2018/08/09 19:02:27

2018/08/09 19:02:27

| voter | sensation |

| author | suweenja |

| permlink | 26yufg-arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives |

| weight | 10000 (100.00%) |

| Transaction Info | Block #24924211/Trx 5fe38aaa4c0dc4610b19a1a5668bf1f5e218c11e |

View Raw JSON Data

{

"trx_id": "5fe38aaa4c0dc4610b19a1a5668bf1f5e218c11e",

"block": 24924211,

"trx_in_block": 2,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2018-08-09T19:02:27",

"op": [

"vote",

{

"voter": "sensation",

"author": "suweenja",

"permlink": "26yufg-arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives",

"weight": 10000

}

]

}suweenjapublished a new post: 26yufg-arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives2018/08/09 15:41:03

suweenjapublished a new post: 26yufg-arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives

2018/08/09 15:41:03

| parent author | |

| parent permlink | bitcoin |

| author | suweenja |

| permlink | 26yufg-arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives |

| title | Arbitrage and Future Potential of Bitcoin Exchange Traded Derivatives |

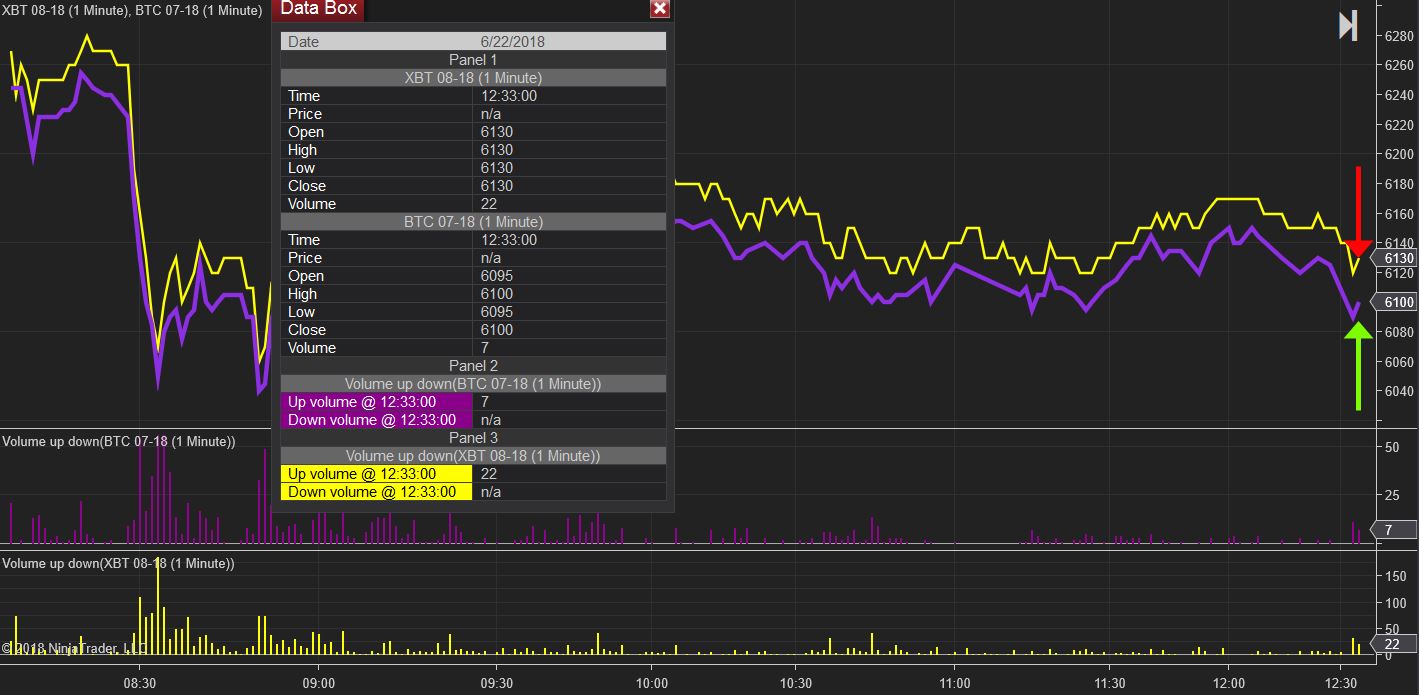

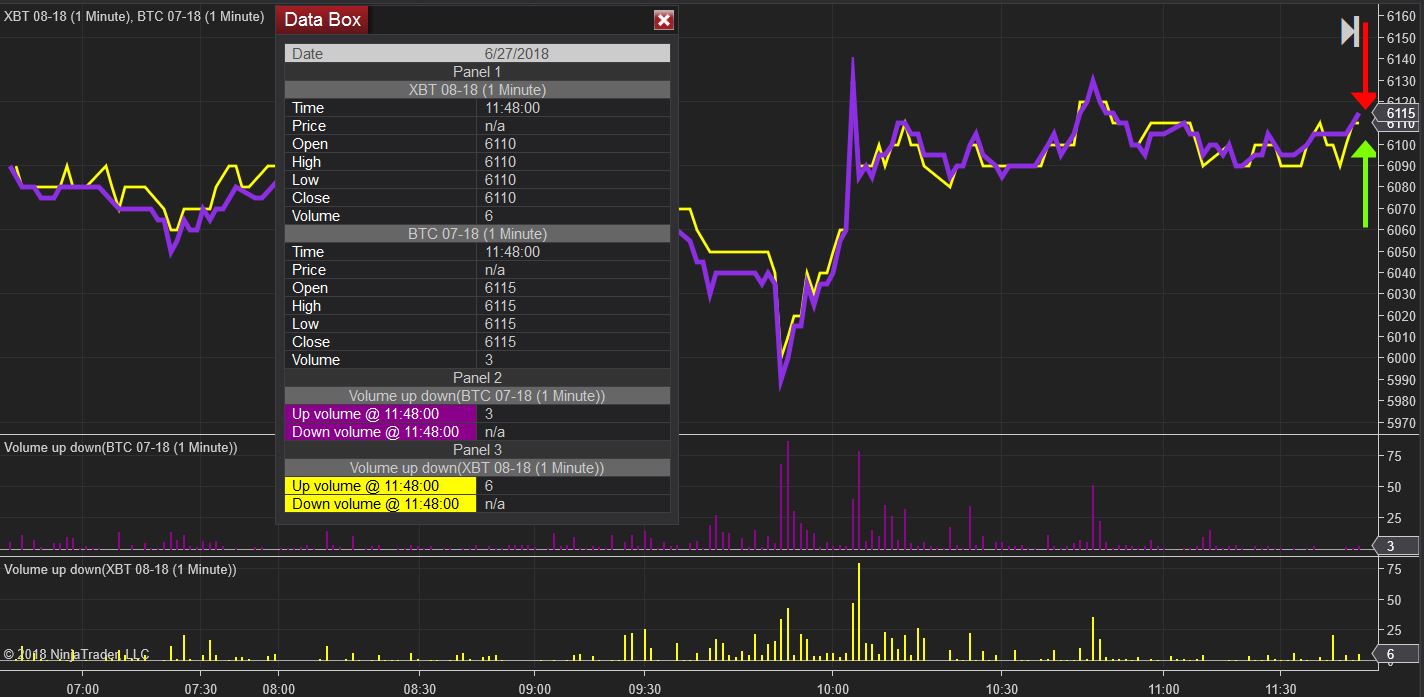

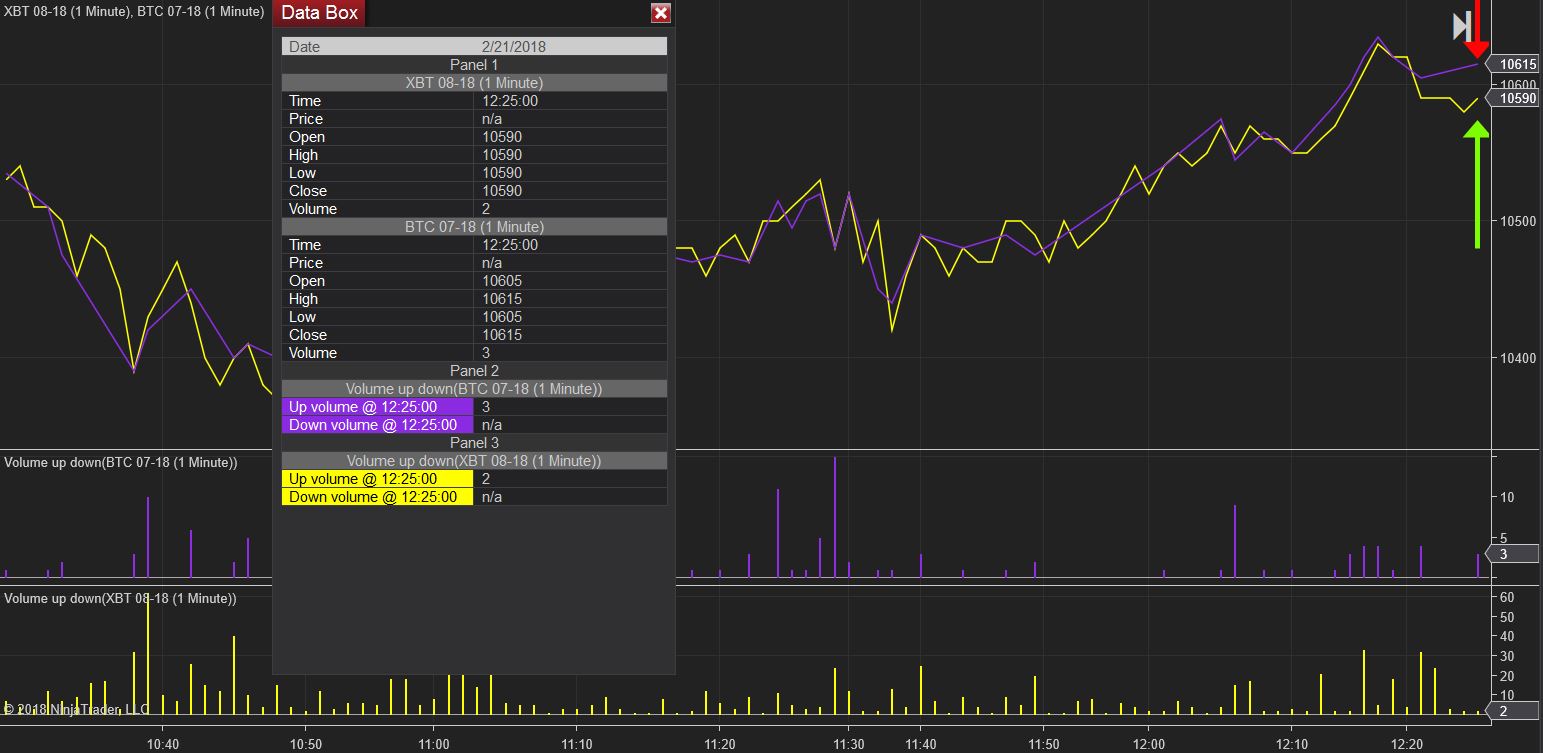

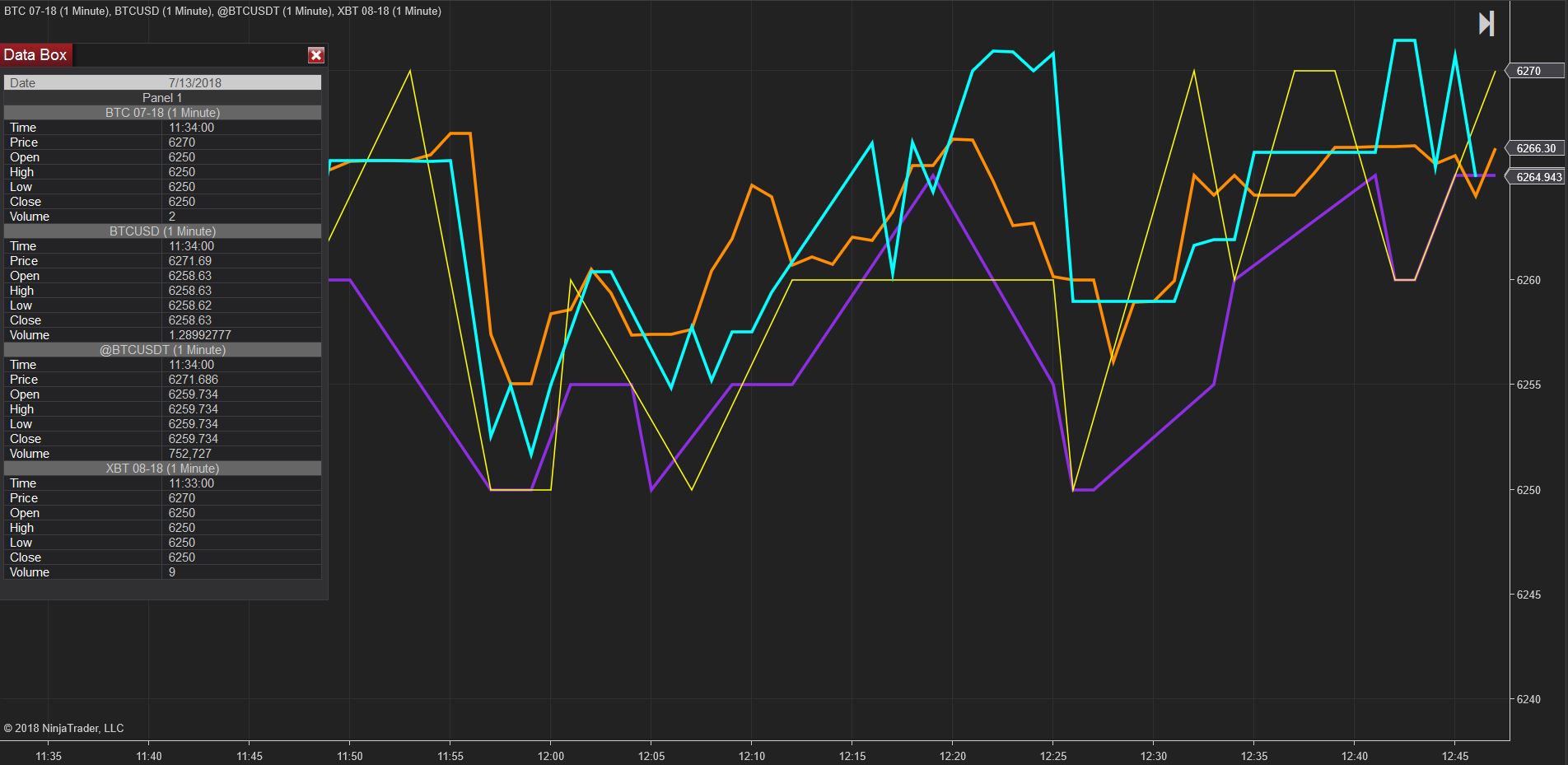

| body | **Trading Thesis** Bitcoin’s exchange traded derivative products currently provide an opportunity for arbitrage or low risk spread trades between the CME’s BTC product and CBOE’s XBT product. Additionally, when traded against the spot Bitcoin markets an additional risk reduction is possible, however there exist several market frictions that make trading this combination of products difficult in practice. The following will quantify the potential opportunity or edge in the future’s spread, then the futures basis trade and last look at some potential new trade opportunities as more exchange traded cryptocurrency derivatives enter the market. **Futures Spread Trades** The futures spread trade is premised on the assumption that after discounting carry differences caused by varying expiration dates, the CME and CBOE futures products should be identical in price. From observation, opportunities when the futures spread prices have diverged significantly, greater than $25, have been infrequent, but considerably more frequent outside of normal US trading hours. Calculations show a $25 spread is the minimum threshold for entering the trade given associated trading fees and margin requirements. Notably, the following calculations can be easily generalized to a specific traders’ fees and situation, but the below rates are representative of a Bitcoin futures market maker. Subject to individual commission rates charged by the futures broker and baring participation in either exchanges market making rebate program, the cheapest trading fees total $4.60 to enter opposite BTC and XBT positions of the same notional. When taking into consideration margin and interest expenses, this increases. Maintenance margin requirements for each product are 43% and 44% of the of the current daily settlement price for the CME and CBOE product respectively. Assuming the current Bitcoin price of $6,600, a risk free rate of 2% and because the futures are not cross margined, to carry this position for a year essentially costs $60 of capital usage or lost profit. The time to expiration between a CBOE and CME contract of the same expiration month averages about 2 weeks, as the CBOE future expires two business days prior to the third Friday of the month and the CME future expires the last Friday of the month. Thus the carry for a 2 week period rounding up is roughly $2.50. In total, the trade costs about $7.10 to put on just in fees and interest. Then assuming you are paying a 2 tick wide ($10) bid-ask spread for each leg, which over time has tightened considerably and will likely continue to, is on average about $20. Thus, the trade per leg costs about $21.42 to enter (20+7.10/5, divided by 5 since the fees calculated were for the entire trade). With an increased risk appetite the minimum threshold can be reduced slightly by avoiding taking liquidity and only providing, however this exposes the strategy to short term price fluctuations when price gaps up or down. The main risk to this spread trade occurs during expiration at which point, it is possible to have built a large inventory of short the expiring future and long the further dated future; since, generally term structure for each product has been in contango. Typically, the cross futures spread reaches a maximum about a week from expiration and decreases as expiration approaches. Simultaneously, this provides an opportunity to trade the calendar spreads of each future or their rolls. Although illiquid, the calendar spread a week out from expiration has for each contract month sold off considerably into expiration. The reasoning behind this is likely explained by an imbalance in the timing of long futures and short futures, i.e., open interest rolling their positions forward. It’s unclear whether this pattern will persist, but a profitable trade historically in BTC & XBT futures has been selling the calendar spread a week or more from expiration and buying it back as close to expiration as possible. Despite liquidity a week out from expiration being relatively low, the same trade in effect is occasionally entered naturally by trading the futures spread in prior weeks. In general, these frictions create an opportunity to enter a cross BTC and XBT futures spread at relatively low risk. The real questions going forward, however as liquidity inevitably improves, is will these same patterns persist. The trade can be seen visually in the below charts. Figure 1 shows the futures spread one week out from expiration of the BTC June contract. The BTC contract is in purple and the XBT contract is in yellow. Here you can buy 1 BTC future at 6100 and sell 5 XBT future at 6130 to initiate the spread trade at $150 difference in notional. Figure 2 shows the spread two days before expiration of the BTC Jun contract. Here you can sell 1 BTC future at 6115 and buy 5 XBT futures at 6110, for another $25 credit. In total the trade lasted four trading days and locked in a profit of $175 less trading fees already discussed from trading the smallest possible quantity in BTC. The pattern is observed to be diminishing over time as Figures 3 & 4 show. The possible profit, before fees from the same strategy at BTC’s February expiration was $400. One important factor to note, that may have led to the diminishing pattern is the CBOE tick increment size was halved from $10.00 to $5.00 ticks on May 7th, 2018. There exist many other situations of this spread occurring especially after normal trading hours, however liquidity can be an issue to put on any sizable spread. Figure 1: Spread 1 week from BTC Jun expiration Yellow=XBT Purple=BTC XBT-BTC=$30  Figure 2: Futures spread 1 day from BTC Jun expiration/roll XBT-BTC= -$5  Figure 3: Spread 1 week from BTC Feb expiration XBT-BTC=$75  Figure 4: Futures spread 1 day from BTC Feb expiration/roll XBT-BTC=-$25  **Basis Trades** A related, but typically more frequent and a wider spread to trade is the basis trade between the Bitcoin futures and spot Bitcoin markets. Assumptions here are that the future expires to the liquid price of Bitcoin across all spot exchanges. For XBT futures, the basis trade is simplified since it is possible to participate in Gemini’s auction to unwind whatever position is left at the same price that the futures settle. However, BTC futures cash settle to the price of Crypto Facilities Bitcoin Reference Rate (BRR) and is not a trade at settlement (TAS) event that allows market participants to offtake excess inventory. The BRR is simply an index aggregating price across constituent exchanges in the last hour before settlement of the future. An additional, issue with BTC basis trading is the contract size equals the price of 5 Bitcoin, unlike XBT’s 1 Bitcoin contract so liquidity in the spot markets is even more critical relatively speaking. These features cause the BTC basis trade to be more risky than XBT, since there will inherently be some slippage to unwinding a sufficiently large BTC futures position into spot Bitcoin. Therefore, the main requirement for basis trading successfully is access to as many spot exchanges and liquidity pools as possible. In practice, the basis fluctuates far more frequently and far quicker than does the futures spread, and is a much more active and involved strategy to run. Thus, an equally important requirement is to have trading technology in place to act quickly on divergence of the future and spot price. In its ideal construction, this technology would be able to instantly determine total possible spot liquidity across all exchanges, calculate a threshold price and volume at which its profitable to enter, and execute trades across these exchanges seamless aggregating trade details in a single platform. Other inputs to this algorithm would include variable trading fees at spot exchanges several of which are volume and side dependent and potentially capitalization expense (ie. moving Bitcoin and or USD between crypto exchanges might be necessary and is not free). The total edge in this trade is the difference in future and spot Bitcoin price, less trading fees and the bid ask spread of each product. As both the futures and spot Bitcoin markets mature from more sophisticated participants entering the space, the basis will inevitably shrink until only the fastest algorithms and technology are competing. Since the creation of the futures products, the basis on a given day has shrunk from easily over ±150 or more to only about on average ±30, which for most market participants is about the breakeven threshold for entering the trade. Generally, only during the most volatile moves or in the most illiquid trading hours for Bitcoin does the basis break well outside of that breakeven range. Figure 5 below displays the basis trade in practice using two charts. In the first chart, we have two spot Bitcoin exchanges, GDAX and Poloniex trading above the price of both futures exchanges on 7/11/2018. Selling 5 GDAX Bitcoin and buying 1 CME BTC here yields a difference in notional of $150. Just two days later on 7/13/2018, the futures and spot exchanges are more or less in line and the trade could be closed to lock in the $150. In practice, it possible there is even more edge in this trade; you could have sold 5 XBT futures here instead of BTC to put on an additional spread against the basis since the XBT was trading $5 higher than the spot exchanges. A keen eye for these trading opportunities still will create profit, but automating the entry and exit of these basis and spread trades could prove orders of magnitude more lucrative. Figure 5: Basis trade July 11th 2018 to July 13th 2018   Outside the scope of CME and CBOE markets, it’s worth noting that crypto futures exchanges like BitMEX and OKEx currently offer similar basis trading opportunities, not only in Bitcoin but other cryptocurrencies as well. Likely, there is more edge in these trades as long as you are able to get preferential trading fees or even rebates to provide the most competitive markets on these exchanges. Additionally, on these exchanges there are interesting and profitable crypto specific trading strategies like hardforks and airdrop arbitrage, where buying a token and shorting its future provides the token holder at no risk, any airdrop tokens’ value, since the future’s value does not include these tokens’ value. **Potential Trades for New Derivative Products** Exchange listed Bitcoin ETFs, options and Altcoin futures are really where traders attentions should be focused moving forward. Altcoin futures are likely to run a similar path to Bitcoin futures, in the sense that the basis trade will for awhile be very profitable, but increasingly quickly compared to Bitcoin futures, will diminish to a breakeven point. If these Altcoin assets ever grow to have ETFs and options derivatives, they will also likely follow a similar path to their Bitcoin derivative counterparts. Bitcoin ETFs are speculated to be right around the corner with the recent CBOE proposal to list and trade VanEck SolidX Bitcoin Trust shares. A Bitcoin ETF would open up the asset class to many more investors and potentially dramatically increase price, but it is the mechanisms behind a potential ETF that are more interesting as a trader. For example, GraniteShares Bitcoin ETF proposal was designed simply to hold front month Bitcoin futures. In its creation this futures ETF structure is the simplest way to gain exposure to the price action of Bitcoin since it does not have to custody Bitcoin, just the regulated and exchanged traded future. An ETF designed in this manner would significantly increase daily turnover on the future as well as the calendar spread during rolls. Just as futures ETFs like USO, UNG and DBA have periodic defined rollovers, a Bitcoin futures ETF would also have mandated times to roll their futures to the subsequent expiration, creating a massive opportunity to trade the rollovers of the ETFs. A simple trade is to provide liquidity or market make the calendar spreads during these rolls and then offtake any accrued inventory after the ETF is finished rolling. Conversely, the physical backed ETF proposal of CBOE to trade VanEck SolidX Bitcoin Trust shares creates a more difficult trading opportunity. Since there's no need to roll futures positions and the ETF holds Bitcoin in ratio with its shares offered, the trading opportunity falls to over-the-counter (OTC) market makers to soak up any edge from the physical ETFs trading activity. This specific ETF proposal intends to use MVIS Bitcoin OTC Index (MVBTCO) to mark to, but this index does not yet exist. Further, it’s unclear who they plan to source liquidity from OTC or on what platform. Possible counterparties could be Circle, Genesis, Cumberland, Jump or several others or by using a liquidity aggregation platform, something along the lines of Omniex. Too much of the details in physically backed ETF proposals’ current states are unclear to generate any specific trading strategy, but what is known is that providing liquidity as an OTC market maker to a major Bitcoin ETF or at least having access to its order flow will be immensely valuable. Last to enter the market, but definitely not least, will be exchange listed options on Bitcoin futures and ETFs. Any trader with the ability to accurately price volatility will have an instant gold mine or should I say, Bitcoin mine. Not only will spreads on these options be huge, but there likely will be no shortage of volatility arbitrage between Bitcoin options on futures, ETFs and spot if liquidity improves or a better venue arises than Deribit or LedgerX. Additionally, traders who can understand and price in the effects of forks, airdrops and other events unique to cryptocurrency will stand to benefit massively. As long as the market matures, liquidity continues to improve and adoption of cryptocurrency grows, the opportunity that comes with the introduction of options from a trader’s perspective is unlimited and preparing for that moment should be the focus of anyone with a long term trading and investment horizon in the space. |

| json metadata | {"tags":["bitcoin","cryptocurrency","exchange","traded","derivatives"],"image":["https://cdn.steemitimages.com/DQmcD96iEfj5mypaZaTs7866Cx6rdD6aytFtYYZ2t8gKo1h/Figure%201%20Good.JPG","https://cdn.steemitimages.com/DQmaFnYXfjUhbzdUP1x5V5sLw9V99jd13AMg29pdW52dwu9/Figure%202%20Good.JPG","https://cdn.steemitimages.com/DQmcrdZPMA6anFQNX4FS8S9QbGsEZKA3Jv3Q8NaXLCwLrts/BTC%20Feb%201%20week%20good.JPG","https://cdn.steemitimages.com/DQmRwprpXeUCHBsnDHbWp5NNfTxKhoKM2tUtoysqzd4oJBS/Feb%20expo%20BTC%202%20days.JPG","https://cdn.steemitimages.com/DQmTLUCvfzyqTCKUvmafmtT2qoJfVikGvXeEujzrHj3TdZn/Figure%203.JPG","https://cdn.steemitimages.com/DQmV8XcuQSPz6Pc8qZLPJ4R9tphoMcoogbKsrKiBFMrRGN6/Figure%204%20Good.JPG"],"app":"steemit/0.1","format":"markdown"} |

| Transaction Info | Block #24920183/Trx f21f0a1a7e04b659e8a9bea0178d63c4df5d6290 |

View Raw JSON Data

{

"trx_id": "f21f0a1a7e04b659e8a9bea0178d63c4df5d6290",

"block": 24920183,

"trx_in_block": 27,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2018-08-09T15:41:03",

"op": [

"comment",

{

"parent_author": "",

"parent_permlink": "bitcoin",

"author": "suweenja",

"permlink": "26yufg-arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives",

"title": "Arbitrage and Future Potential of Bitcoin Exchange Traded Derivatives",

"body": "**Trading Thesis**\nBitcoin’s exchange traded derivative products currently provide an opportunity for arbitrage or low risk spread trades between the CME’s BTC product and CBOE’s XBT product. Additionally, when traded against the spot Bitcoin markets an additional risk reduction is possible, however there exist several market frictions that make trading this combination of products difficult in practice. The following will quantify the potential opportunity or edge in the future’s spread, then the futures basis trade and last look at some potential new trade opportunities as more exchange traded cryptocurrency derivatives enter the market. \n\n**Futures Spread Trades**\nThe futures spread trade is premised on the assumption that after discounting carry differences caused by varying expiration dates, the CME and CBOE futures products should be identical in price. From observation, opportunities when the futures spread prices have diverged significantly, greater than $25, have been infrequent, but considerably more frequent outside of normal US trading hours. Calculations show a $25 spread is the minimum threshold for entering the trade given associated trading fees and margin requirements. Notably, the following calculations can be easily generalized to a specific traders’ fees and situation, but the below rates are representative of a Bitcoin futures market maker. \n\nSubject to individual commission rates charged by the futures broker and baring participation in either exchanges market making rebate program, the cheapest trading fees total $4.60 to enter opposite BTC and XBT positions of the same notional. When taking into consideration margin and interest expenses, this increases. Maintenance margin requirements for each product are 43% and 44% of the of the current daily settlement price for the CME and CBOE product respectively. Assuming the current Bitcoin price of $6,600, a risk free rate of 2% and because the futures are not cross margined, to carry this position for a year essentially costs $60 of capital usage or lost profit. The time to expiration between a CBOE and CME contract of the same expiration month averages about 2 weeks, as the CBOE future expires two business days prior to the third Friday of the month and the CME future expires the last Friday of the month. Thus the carry for a 2 week period rounding up is roughly $2.50. In total, the trade costs about $7.10 to put on just in fees and interest. Then assuming you are paying a 2 tick wide ($10) bid-ask spread for each leg, which over time has tightened considerably and will likely continue to, is on average about $20. Thus, the trade per leg costs about $21.42 to enter (20+7.10/5, divided by 5 since the fees calculated were for the entire trade). With an increased risk appetite the minimum threshold can be reduced slightly by avoiding taking liquidity and only providing, however this exposes the strategy to short term price fluctuations when price gaps up or down. \n\nThe main risk to this spread trade occurs during expiration at which point, it is possible to have built a large inventory of short the expiring future and long the further dated future; since, generally term structure for each product has been in contango. Typically, the cross futures spread reaches a maximum about a week from expiration and decreases as expiration approaches. Simultaneously, this provides an opportunity to trade the calendar spreads of each future or their rolls. Although illiquid, the calendar spread a week out from expiration has for each contract month sold off considerably into expiration. The reasoning behind this is likely explained by an imbalance in the timing of long futures and short futures, i.e., open interest rolling their positions forward. It’s unclear whether this pattern will persist, but a profitable trade historically in BTC & XBT futures has been selling the calendar spread a week or more from expiration and buying it back as close to expiration as possible. Despite liquidity a week out from expiration being relatively low, the same trade in effect is occasionally entered naturally by trading the futures spread in prior weeks. In general, these frictions create an opportunity to enter a cross BTC and XBT futures spread at relatively low risk. The real questions going forward, however as liquidity inevitably improves, is will these same patterns persist.\n\nThe trade can be seen visually in the below charts. Figure 1 shows the futures spread one week out from expiration of the BTC June contract. The BTC contract is in purple and the XBT contract is in yellow. Here you can buy 1 BTC future at 6100 and sell 5 XBT future at 6130 to initiate the spread trade at $150 difference in notional. Figure 2 shows the spread two days before expiration of the BTC Jun contract. Here you can sell 1 BTC future at 6115 and buy 5 XBT futures at 6110, for another $25 credit. In total the trade lasted four trading days and locked in a profit of $175 less trading fees already discussed from trading the smallest possible quantity in BTC. The pattern is observed to be diminishing over time as Figures 3 & 4 show. The possible profit, before fees from the same strategy at BTC’s February expiration was $400. One important factor to note, that may have led to the diminishing pattern is the CBOE tick increment size was halved from $10.00 to $5.00 ticks on May 7th, 2018. There exist many other situations of this spread occurring especially after normal trading hours, however liquidity can be an issue to put on any sizable spread. \n\nFigure 1: Spread 1 week from BTC Jun expiration Yellow=XBT Purple=BTC XBT-BTC=$30\n\n\nFigure 2: Futures spread 1 day from BTC Jun expiration/roll XBT-BTC= -$5\n\n\nFigure 3: Spread 1 week from BTC Feb expiration XBT-BTC=$75\n\n\nFigure 4: Futures spread 1 day from BTC Feb expiration/roll XBT-BTC=-$25\n\n\n**Basis Trades**\n\tA related, but typically more frequent and a wider spread to trade is the basis trade between the Bitcoin futures and spot Bitcoin markets. Assumptions here are that the future expires to the liquid price of Bitcoin across all spot exchanges. For XBT futures, the basis trade is simplified since it is possible to participate in Gemini’s auction to unwind whatever position is left at the same price that the futures settle. However, BTC futures cash settle to the price of Crypto Facilities Bitcoin Reference Rate (BRR) and is not a trade at settlement (TAS) event that allows market participants to offtake excess inventory. The BRR is simply an index aggregating price across constituent exchanges in the last hour before settlement of the future. An additional, issue with BTC basis trading is the contract size equals the price of 5 Bitcoin, unlike XBT’s 1 Bitcoin contract so liquidity in the spot markets is even more critical relatively speaking.\n\nThese features cause the BTC basis trade to be more risky than XBT, since there will inherently be some slippage to unwinding a sufficiently large BTC futures position into spot Bitcoin. Therefore, the main requirement for basis trading successfully is access to as many spot exchanges and liquidity pools as possible. In practice, the basis fluctuates far more frequently and far quicker than does the futures spread, and is a much more active and involved strategy to run. Thus, an equally important requirement is to have trading technology in place to act quickly on divergence of the future and spot price. In its ideal construction, this technology would be able to instantly determine total possible spot liquidity across all exchanges, calculate a threshold price and volume at which its profitable to enter, and execute trades across these exchanges seamless aggregating trade details in a single platform. Other inputs to this algorithm would include variable trading fees at spot exchanges several of which are volume and side dependent and potentially capitalization expense (ie. moving Bitcoin and or USD between crypto exchanges might be necessary and is not free). \n\nThe total edge in this trade is the difference in future and spot Bitcoin price, less trading fees and the bid ask spread of each product. As both the futures and spot Bitcoin markets mature from more sophisticated participants entering the space, the basis will inevitably shrink until only the fastest algorithms and technology are competing. Since the creation of the futures products, the basis on a given day has shrunk from easily over ±150 or more to only about on average ±30, which for most market participants is about the breakeven threshold for entering the trade. Generally, only during the most volatile moves or in the most illiquid trading hours for Bitcoin does the basis break well outside of that breakeven range. \n\nFigure 5 below displays the basis trade in practice using two charts. In the first chart, we have two spot Bitcoin exchanges, GDAX and Poloniex trading above the price of both futures exchanges on 7/11/2018. Selling 5 GDAX Bitcoin and buying 1 CME BTC here yields a difference in notional of $150. Just two days later on 7/13/2018, the futures and spot exchanges are more or less in line and the trade could be closed to lock in the $150. In practice, it possible there is even more edge in this trade; you could have sold 5 XBT futures here instead of BTC to put on an additional spread against the basis since the XBT was trading $5 higher than the spot exchanges. A keen eye for these trading opportunities still will create profit, but automating the entry and exit of these basis and spread trades could prove orders of magnitude more lucrative.\n\nFigure 5: Basis trade July 11th 2018 to July 13th 2018\n\n\n\nOutside the scope of CME and CBOE markets, it’s worth noting that crypto futures exchanges like BitMEX and OKEx currently offer similar basis trading opportunities, not only in Bitcoin but other cryptocurrencies as well. Likely, there is more edge in these trades as long as you are able to get preferential trading fees or even rebates to provide the most competitive markets on these exchanges. Additionally, on these exchanges there are interesting and profitable crypto specific trading strategies like hardforks and airdrop arbitrage, where buying a token and shorting its future provides the token holder at no risk, any airdrop tokens’ value, since the future’s value does not include these tokens’ value.\n\n**Potential Trades for New Derivative Products**\nExchange listed Bitcoin ETFs, options and Altcoin futures are really where traders attentions should be focused moving forward. Altcoin futures are likely to run a similar path to Bitcoin futures, in the sense that the basis trade will for awhile be very profitable, but increasingly quickly compared to Bitcoin futures, will diminish to a breakeven point. If these Altcoin assets ever grow to have ETFs and options derivatives, they will also likely follow a similar path to their Bitcoin derivative counterparts.\n\nBitcoin ETFs are speculated to be right around the corner with the recent CBOE proposal to list and trade VanEck SolidX Bitcoin Trust shares. A Bitcoin ETF would open up the asset class to many more investors and potentially dramatically increase price, but it is the mechanisms behind a potential ETF that are more interesting as a trader. For example, GraniteShares Bitcoin ETF proposal was designed simply to hold front month Bitcoin futures. In its creation this futures ETF structure is the simplest way to gain exposure to the price action of Bitcoin since it does not have to custody Bitcoin, just the regulated and exchanged traded future. An ETF designed in this manner would significantly increase daily turnover on the future as well as the calendar spread during rolls. Just as futures ETFs like USO, UNG and DBA have periodic defined rollovers, a Bitcoin futures ETF would also have mandated times to roll their futures to the subsequent expiration, creating a massive opportunity to trade the rollovers of the ETFs. A simple trade is to provide liquidity or market make the calendar spreads during these rolls and then offtake any accrued inventory after the ETF is finished rolling. \n\nConversely, the physical backed ETF proposal of CBOE to trade VanEck SolidX Bitcoin Trust shares creates a more difficult trading opportunity. Since there's no need to roll futures positions and the ETF holds Bitcoin in ratio with its shares offered, the trading opportunity falls to over-the-counter (OTC) market makers to soak up any edge from the physical ETFs trading activity. This specific ETF proposal intends to use MVIS Bitcoin OTC Index (MVBTCO) to mark to, but this index does not yet exist. Further, it’s unclear who they plan to source liquidity from OTC or on what platform. Possible counterparties could be Circle, Genesis, Cumberland, Jump or several others or by using a liquidity aggregation platform, something along the lines of Omniex. Too much of the details in physically backed ETF proposals’ current states are unclear to generate any specific trading strategy, but what is known is that providing liquidity as an OTC market maker to a major Bitcoin ETF or at least having access to its order flow will be immensely valuable.\n\n\tLast to enter the market, but definitely not least, will be exchange listed options on Bitcoin futures and ETFs. Any trader with the ability to accurately price volatility will have an instant gold mine or should I say, Bitcoin mine. Not only will spreads on these options be huge, but there likely will be no shortage of volatility arbitrage between Bitcoin options on futures, ETFs and spot if liquidity improves or a better venue arises than Deribit or LedgerX. Additionally, traders who can understand and price in the effects of forks, airdrops and other events unique to cryptocurrency will stand to benefit massively. As long as the market matures, liquidity continues to improve and adoption of cryptocurrency grows, the opportunity that comes with the introduction of options from a trader’s perspective is unlimited and preparing for that moment should be the focus of anyone with a long term trading and investment horizon in the space.",

"json_metadata": "{\"tags\":[\"bitcoin\",\"cryptocurrency\",\"exchange\",\"traded\",\"derivatives\"],\"image\":[\"https://cdn.steemitimages.com/DQmcD96iEfj5mypaZaTs7866Cx6rdD6aytFtYYZ2t8gKo1h/Figure%201%20Good.JPG\",\"https://cdn.steemitimages.com/DQmaFnYXfjUhbzdUP1x5V5sLw9V99jd13AMg29pdW52dwu9/Figure%202%20Good.JPG\",\"https://cdn.steemitimages.com/DQmcrdZPMA6anFQNX4FS8S9QbGsEZKA3Jv3Q8NaXLCwLrts/BTC%20Feb%201%20week%20good.JPG\",\"https://cdn.steemitimages.com/DQmRwprpXeUCHBsnDHbWp5NNfTxKhoKM2tUtoysqzd4oJBS/Feb%20expo%20BTC%202%20days.JPG\",\"https://cdn.steemitimages.com/DQmTLUCvfzyqTCKUvmafmtT2qoJfVikGvXeEujzrHj3TdZn/Figure%203.JPG\",\"https://cdn.steemitimages.com/DQmV8XcuQSPz6Pc8qZLPJ4R9tphoMcoogbKsrKiBFMrRGN6/Figure%204%20Good.JPG\"],\"app\":\"steemit/0.1\",\"format\":\"markdown\"}"

}

]

}suweenjapublished a new post: arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives2018/07/27 20:44:36

suweenjapublished a new post: arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives

2018/07/27 20:44:36

| parent author | |

| parent permlink | bitcoin |

| author | suweenja |

| permlink | arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives |

| title | Deleted |

| body | Deleted |

| json metadata | {"tags":["deleted","bitcoin"],"app":"steemit/0.1","format":"markdown"} |

| Transaction Info | Block #24552436/Trx 04366010824a4a7c8a77d541253802a1e6452220 |

View Raw JSON Data

{

"trx_id": "04366010824a4a7c8a77d541253802a1e6452220",

"block": 24552436,

"trx_in_block": 12,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2018-07-27T20:44:36",

"op": [

"comment",

{

"parent_author": "",

"parent_permlink": "bitcoin",

"author": "suweenja",

"permlink": "arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives",

"title": "Deleted",

"body": "Deleted",

"json_metadata": "{\"tags\":[\"deleted\",\"bitcoin\"],\"app\":\"steemit/0.1\",\"format\":\"markdown\"}"

}

]

}suweenjapublished a new post: arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives2018/07/27 20:42:30

suweenjapublished a new post: arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives

2018/07/27 20:42:30

| parent author | |

| parent permlink | bitcoin |

| author | suweenja |

| permlink | arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives |

| title | Spam |

| body | Deleted |

| json metadata | {"tags":["deleted","bitcoin"],"app":"steemit/0.1","format":"markdown"} |

| Transaction Info | Block #24552394/Trx 30ce091cae7770c68f87723025f10b36f3336bf5 |

View Raw JSON Data

{

"trx_id": "30ce091cae7770c68f87723025f10b36f3336bf5",

"block": 24552394,

"trx_in_block": 48,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2018-07-27T20:42:30",

"op": [

"comment",

{

"parent_author": "",

"parent_permlink": "bitcoin",

"author": "suweenja",

"permlink": "arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives",

"title": "Spam",

"body": "Deleted",

"json_metadata": "{\"tags\":[\"deleted\",\"bitcoin\"],\"app\":\"steemit/0.1\",\"format\":\"markdown\"}"

}

]

}suweenjapublished a new post: arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives2018/07/27 20:39:33

suweenjapublished a new post: arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives

2018/07/27 20:39:33

| parent author | |

| parent permlink | bitcoin |

| author | suweenja |

| permlink | arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives |

| title | Arbitrage and Future Potential of Bitcoin Exchange Traded Derivatives |

| body | **Trading Thesis** Bitcoin’s exchange traded derivative products currently provide an opportunity for arbitrage or low risk spread trades between the CME’s BTC product and CBOE’s XBT product. Additionally, when traded against the spot Bitcoin markets an additional risk reduction is possible, however there exist several market frictions that make trading this combination of products difficult in practice. The following will quantify the potential opportunity or edge in the future’s spread, then the futures basis trade and last look at some potential new trade opportunities as more exchange traded cryptocurrency derivatives enter the market. **Futures Spread Trades** The futures spread trade is premised on the assumption that after discounting carry differences caused by varying expiration dates, the CME and CBOE futures products should be identical in price. From experience, opportunities when the futures spread prices have diverged significantly, greater than $25, have been infrequent, but considerably more frequent outside of normal US trading hours. Calculations show a $25 spread is the minimum threshold for entering the trade given associated trading fees and margin requirements. Notably, the following calculations can be easily generalized to a specific traders’ fees and situation, but the below rates are representative of a Bitcoin futures market maker. Subject to individual commission rates charged by the futures broker and baring participation in either exchanges market making rebate program, the cheapest trading fees total $4.60 to enter opposite BTC and XBT positions of the same notional. When taking into consideration margin and interest expenses, this increases. Maintenance margin requirements for each product are 43% and 44% of the of the current daily settlement price for the CME and CBOE product respectively. Assuming the current Bitcoin price of $6,600, a risk free rate of 2% and because the futures are not cross margined, to carry this position for a year essentially costs $60 of capital usage or lost profit. The time to expiration between a CBOE and CME contract of the same expiration month averages about 2 weeks, as the CBOE future expires two business days prior to the third Friday of the month and the CME future expires the last Friday of the month. Thus the carry for a 2 week period rounding up is roughly $2.50. In total, the trade costs about $7.10 to put on just in fees and interest. Then assuming you are paying a 2 tick wide ($10) bid-ask spread for each leg, which over time has tightened considerably and will likely continue to, is on average about $20. Thus, the trade per leg costs about $21.42 to enter (20+7.10/5, divided by 5 since the fees calculated were for the entire trade). With an increased risk appetite the minimum threshold can be reduced slightly by avoiding taking liquidity and only providing, however this exposes the strategy to short term price fluctuations when price gaps up or down. The main risk to this spread trade occurs during expiration at which point, it is possible to have built a large inventory of short the expiring future and long the further dated future; since, generally term structure for each product has been in contango. Typically, the cross futures spread reaches a maximum about a week from expiration and decreases as expiration approaches. Simultaneously, this provides an opportunity to trade the calendar spreads of each future or their rolls. Here’s where experience in this nascent market proves valuable; although illiquid, the calendar spread a week out from expiration has for each contract month sold off considerably into expiration. The reasoning behind this is likely explained by an imbalance in the timing of long futures and short futures, i.e., open interest rolling their positions forward. It’s unclear whether this pattern will persist, but a profitable trade historically in BTC & XBT futures has been selling the calendar spread a week or more from expiration and buying it back as close to expiration as possible. Despite liquidity a week out from expiration being relatively low, the same trade in effect is occasionally entered naturally by trading the futures spread in prior weeks. In general, these frictions create an opportunity to enter a cross BTC and XBT futures spread at relatively low risk. The real questions going forward, however as liquidity inevitably improves, is will these same patterns persist. The trade can be seen visually in the below charts. Figure 1 shows the futures spread one week out from expiration of the BTC June contract. The BTC contract is in purple and the XBT contract is in yellow. Here you can buy 1 BTC future at 6100 and sell 5 XBT future at 6130 to initiate the spread trade at $150 difference in notional. Figure 2 shows the spread two days before expiration of the BTC Jun contract. Here you can sell 1 BTC future at 6115 and buy 5 XBT futures at 6110, for another $25 credit. In total the trade lasted four trading days and locked in a profit of $175 less trading fees already discussed from trading the smallest possible quantity in BTC. The pattern is observed to be diminishing over time as Figures 3 & 4 show. The possible profit, before fees from the same strategy at BTC’s February expiration was $400. From experience, there are many other situations of this spread occurring especially after normal trading hours, however liquidity can be an issue to put on any sizable spread. Figure 1: Spread 1 week from BTC Jun expiration Yellow=XBT Purple=BTC XBT-BTC=$30  Figure 2: Futures spread 1 day from BTC Jun expiration/roll XBT-BTC= -$5  Figure 3: Spread 1 week from BTC Feb expiration XBT-BTC=$75  Figure 4: Futures spread 1 day from BTC Feb expiration/roll XBT-BTC=-$5  **Basis Trades** A related, but typically more frequent and a wider spread to trade is the basis trade between the Bitcoin futures and spot Bitcoin markets. Assumptions here are that the future expires to the liquid price of Bitcoin across all spot exchanges. For XBT futures, the basis trade is simplified since it is possible to participate in Gemini’s auction to unwind whatever position is left at the same price that the futures settle. However, BTC futures cash settle to the price of Crypto Facilities Bitcoin Reference Rate (BRR) and is not a trade at settlement (TAS) event that allows market participants to offtake excess inventory. The BRR is simply an index aggregating price across constituent exchanges in the last hour before settlement of the future. An additional, issue with BTC basis trading is the contract size equals the price of 5 Bitcoin, unlike XBT’s 1 Bitcoin contract so liquidity in the spot markets is even more critical relatively speaking. These features cause the BTC basis trade to be more risky than XBT, since there will inherently be some slippage to unwinding a sufficiently large BTC futures position into spot Bitcoin. Therefore, the main requirement for basis trading successfully is access to as many spot exchanges and liquidity pools as possible. In practice, the basis fluctuates far more frequently and far quicker than does the futures spread, and is a much more active and involved strategy to run. Thus, an equally important requirement is to have trading technology in place to act quickly on divergence of the future and spot price. In its ideal construction, this technology would be able to instantly determine total possible spot liquidity across all exchanges, calculate a threshold price and volume at which its profitable to enter, and execute trades across these exchanges seamless aggregating trade details in a single platform. Other inputs to this algorithm would include variable trading fees at spot exchanges several of which are volume and side dependent and potentially capitalization expense (ie. moving Bitcoin and or USD between crypto exchanges might be necessary and is not free). The total edge in this trade is the difference in future and spot Bitcoin price, less trading fees and the bid ask spread of each product. As both the futures and spot Bitcoin markets mature from more sophisticated participants entering the space, the basis will inevitably shrink until only the fastest algorithms and technology are competing. Since the creation of the futures products, the basis on a given day has shrunk from easily over ±150 or more to only about on average ±30, which for most market participants is about the breakeven threshold for entering the trade. Generally, only during the most volatile moves or in the most illiquid trading hours for Bitcoin does the basis break well outside of that breakeven range. Figure 5 below displays the basis trade in practice using two charts. In the first chart, we have two spot Bitcoin exchanges, GDAX and Poloniex trading above the price of both futures exchanges on 7/11/2018. Selling 5 GDAX Bitcoin and buying 1 CME BTC here yields a difference in notional of $150. Just two days later on 7/13/2018, the futures and spot exchanges are more or less in line and the trade could be closed to lock in the $150. In practice, it possible there is even more edge in this trade; you could have sold 5 XBT futures here instead of BTC to put on an additional spread against the basis since the XBT was trading $5 higher than the spot exchanges. A keen eye for these trading opportunities still will create profit, but automating the entry and exit of these basis and spread trades could prove orders of magnitude more lucrative. Figure 5: Basis trade July 11th 2018 to July 13th 2018   Outside the scope of CME and CBOE markets, it’s worth noting that crypto futures exchanges like BitMEX and OKEx currently offer similar basis trading opportunities, not only in Bitcoin but other cryptocurrencies as well. Likely, there is more edge in these trades as long as you are able to get preferential trading fees or even rebates to provide the most competitive markets on these exchanges. Additionally, on these exchanges there are interesting and profitable crypto specific trading strategies like hardforks and airdrop arbitrage, where buying a token and shorting its future provides the token holder at no risk, any airdrop tokens’ value, since the future’s value does not include these tokens’ value. **Potential Trades for New Derivative Products** Exchange listed Bitcoin ETFs, options and Altcoin futures are really where traders attentions should be focused moving forward. Altcoin futures are likely to run a similar path to Bitcoin futures, in the sense that the basis trade will for awhile be very profitable, but increasingly quickly compared to Bitcoin futures, will diminish to a breakeven point. If these Altcoin assets ever grow to have ETFs and options derivatives, they will also likely follow a similar path to their Bitcoin derivative counterparts. Bitcoin ETFs are speculated to be right around the corner with the recent CBOE proposal to list and trade VanEck SolidX Bitcoin Trust shares. A Bitcoin ETF would open up the asset class to many more investors and potentially dramatically increase price, but it is the mechanisms behind a potential ETF that are more interesting as a trader. For example, GraniteShares Bitcoin ETF proposal was designed simply to hold front month Bitcoin futures. In its creation this futures ETF structure is the simplest way to gain exposure to the price action of Bitcoin since it does not have to custody Bitcoin, just the regulated and exchanged traded future. An ETF designed in this manner would significantly increase daily turnover on the future as well as the calendar spread during rolls. Just as futures ETFs like USO, UNG and DBA have periodic defined rollovers, a Bitcoin futures ETF would also have mandated times to roll their futures to the subsequent expiration, creating a massive opportunity to trade the rollovers of the ETFs. A simple trade is to provide liquidity or market make the calendar spreads during these rolls and then offtake any accrued inventory after the ETF is finished rolling. Conversely, the physical backed ETF proposal of CBOE to trade VanEck SolidX Bitcoin Trust shares creates a more difficult trading opportunity. Since there's no need to roll futures positions and the ETF holds Bitcoin in ratio with its shares offered, the trading opportunity falls to over-the-counter (OTC) market makers to soak up any edge from the physical ETFs trading activity. This specific ETF proposal intends to use MVIS Bitcoin OTC Index (MVBTCO) to mark to, but this index does not yet exist. Further, it’s unclear who they plan to source liquidity from OTC or on what platform. Possible counterparties could be Circle, Genesis, Cumberland, Jump or several others or by using a liquidity aggregation platform, something along the lines of Omniex. Too much of the details in physically backed ETF proposals’ current states are unclear to generate any specific trading strategy, but what is known is that providing liquidity as an OTC market maker to a major Bitcoin ETF or at least having access to its order flow will be immensely valuable. Last to enter the market, but definitely not least, will be exchange listed options on Bitcoin futures and ETFs. Any trader with the ability to accurately price volatility will have an instant gold mine or should I say, Bitcoin mine. Not only will spreads on these options be huge, but there likely will be no shortage of volatility arbitrage between Bitcoin options on futures, ETFs and spot if liquidity improves or a better venue arises than Deribit or LedgerX. Additionally, traders who can understand and price in the effects of forks, airdrops and other events unique to cryptocurrency will stand to benefit massively. As long as the market matures, liquidity continues to improve and adoption of cryptocurrency grows, the opportunity that comes with the introduction of options from a trader’s perspective is unlimited and preparing for that moment should be the focus of anyone with a long term trading and investment horizon in the space. |

| json metadata | {"tags":["bitcoin","futures","arbitrage","cryptocurrency","btc"],"image":["https://cdn.steemitimages.com/DQmcD96iEfj5mypaZaTs7866Cx6rdD6aytFtYYZ2t8gKo1h/Figure%201%20Good.JPG","https://cdn.steemitimages.com/DQmaFnYXfjUhbzdUP1x5V5sLw9V99jd13AMg29pdW52dwu9/Figure%202%20Good.JPG","https://cdn.steemitimages.com/DQmcrdZPMA6anFQNX4FS8S9QbGsEZKA3Jv3Q8NaXLCwLrts/BTC%20Feb%201%20week%20good.JPG","https://cdn.steemitimages.com/DQmRwprpXeUCHBsnDHbWp5NNfTxKhoKM2tUtoysqzd4oJBS/Feb%20expo%20BTC%202%20days.JPG","https://cdn.steemitimages.com/DQmTLUCvfzyqTCKUvmafmtT2qoJfVikGvXeEujzrHj3TdZn/Figure%203.JPG","https://cdn.steemitimages.com/DQmV8XcuQSPz6Pc8qZLPJ4R9tphoMcoogbKsrKiBFMrRGN6/Figure%204%20Good.JPG"],"app":"steemit/0.1","format":"markdown"} |

| Transaction Info | Block #24552335/Trx a97eafd04743bdf14d1a49fe48db8e8a28e42a53 |

View Raw JSON Data

{

"trx_id": "a97eafd04743bdf14d1a49fe48db8e8a28e42a53",

"block": 24552335,

"trx_in_block": 26,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2018-07-27T20:39:33",

"op": [

"comment",

{

"parent_author": "",

"parent_permlink": "bitcoin",

"author": "suweenja",

"permlink": "arbitrage-and-future-potential-of-bitcoin-exchange-traded-derivatives",

"title": "Arbitrage and Future Potential of Bitcoin Exchange Traded Derivatives",